Watch Nicola & Azlan in their 2 minute take on the investment opportunities in Indonesia.

Indonesia has entered the spotlight as a key investment destination for foreign investors, driven by the Indonesian government opening foreign investment in key sectors and actively touting the privatisation of assets including critical infrastructure and clean energy.

Professionals who specialise in transactional work in Indonesia have welcomed this well overdue pivot.

How can foreign investors best protect themselves whilst also maximising deal execution when investing into Indonesia?

In this insight, King & Wood Mallesons shares:

- What has changed in the Indonesian legal and regulatory environment

- What foreign investors need to know about the investment opportunities in Indonesia

- How to maximise deal certainty when investing into Indonesia.

- Foreign investors are circling opportunities in Indonesia as its economy opens

- Indonesia lifted foreign investment restrictions across a range of sectors in 2020

- Investments have surged, including Macquarie’s $610m investment into Bersama Digital Infrastructure and BDx’s $300m joint venture with Indosat Ooredoo Hutchison and Lintasarta

- Indonesia’s new sovereign wealth fund and pending carbon trading mechanism will also drive investment

- To conform with global standards and protect foreign investors, it is important to engage a local partner, conduct due diligence and check governance among other considerations

Why Indonesia

The largest economy in ASEAN

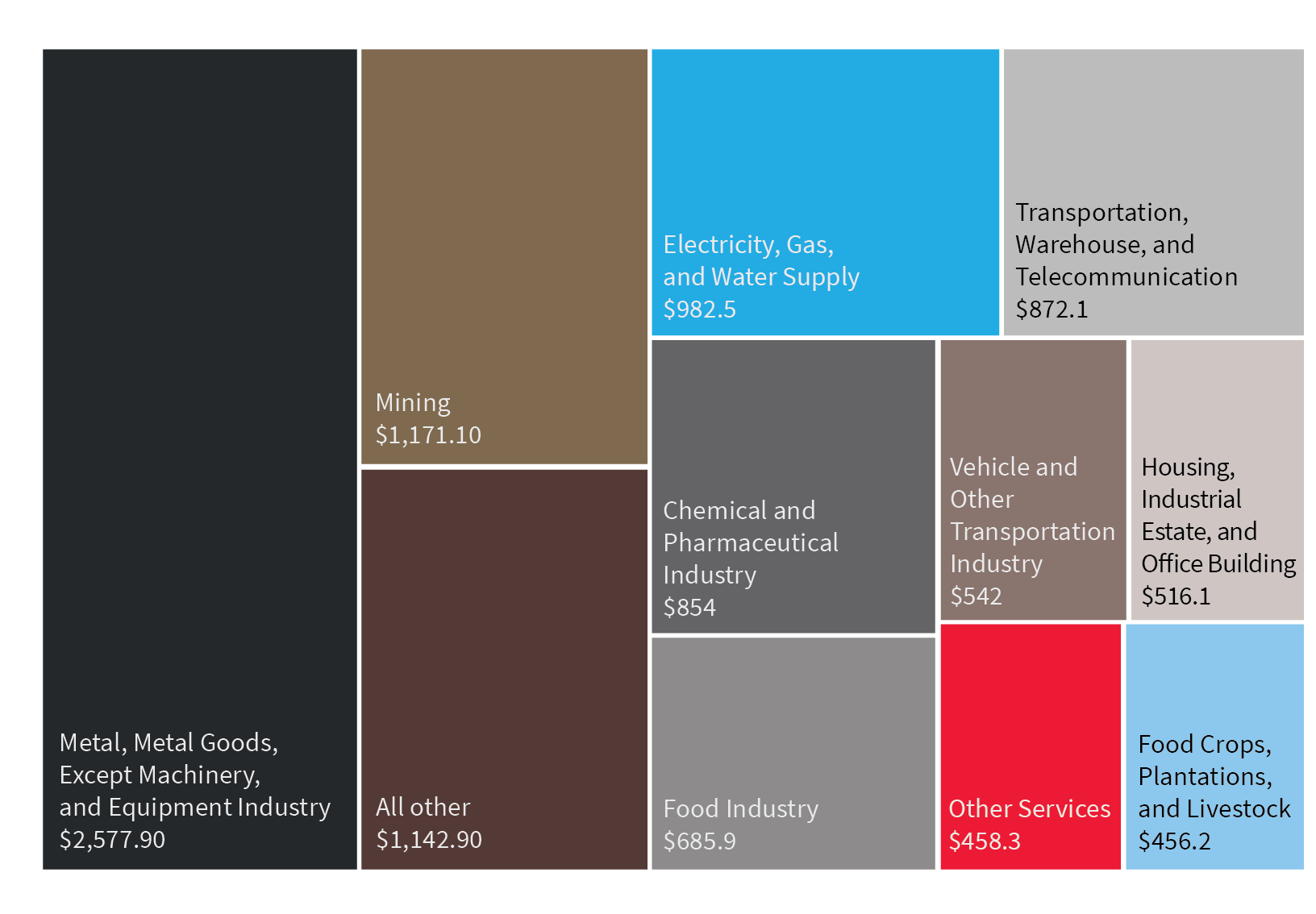

Indonesia’s engine is traditionally powered by a large mining and natural resources sector and agricultural sector. Foreign direct investment is dominated by mining, metals and electricity according to statistics published by Indonesia’s investment coordinating board, the Badan Koordinasi Penanaman Modal (BKPM). Indonesia’s deep reserves of iron-ore and coal help power the Asian manufacturing powerhouses around it such as China, Japan and India, as well as the rising Malaysia. Indonesia’s extraction and exportation of palm oil has also historically been very lucrative, feeding the same manufacturing powerhouses regionally and across to Europe.

Source: BKPM, Investment Realisation, Q1 2022

Expanding focus beyond mining and agriculture to infrastructure, manufacturing & more

This is not to say that Indonesia is a two-trick pony. The Indonesian government recently released its list of government focus sectors, seeking to deleverage its over-reliance on mining and natural resources and agricultural exports. This diversification reflects the Indonesian government’s reading of global economic headwinds and surging climate temperatures. Harsh lessons have also been learnt from recent volatility in commodity prices.

Unsurprisingly, infrastructure is a key focus, given Indonesia’s rapid growth, rising middle class and liberalisation of its economy. First class infrastructure is needed to support and sustain the frenetic pace in which Indonesia is now demanding goods and services and conducting business. Indonesia’s new sovereign wealth fund, the Lembaga Pengelola Investasi (LPI) will play a key role in this (see further below). Other areas of focus for the Indonesian government are manufacturing, maritime industries and tourism.

Changing demographics increases wealth

Another key aspect driving Indonesia’s rapid growth is its rising middle class and its round-the-clock use of technology.[1] Generational economic growth in Indonesia has resulted in a middle class in Indonesia that is high-income earning, well-educated, and worldly. This shift in demographics has ignited demand for sophisticated goods and services across a wide range of industries and adds to an attractive business case for foreign investors.

Indonesia has per-capita one of the highest percentages of smartphone usage in the world. Everyday goods and services are ordered via smartphone. The recent merger between Gojek (a ride-hailing app) and Tokopedia (an e-commerce platform) to create a combined Indonesian business valued at approximately US$18 billion is an example of these underlying demographic factors driving extraordinary outcomes in the Indonesian business world.

Recent liberalisation of the economy

The legal and regulatory environment in Indonesia has also shifted to one encouraging in-bound foreign investment. The introduction of a range of measures under the Omnibus Law has had an extraordinary impact on the Indonesian economy and positions Indonesian well to strike at new opportunities which are presenting themselves.

INSEAD, “Southeast Asia VC Healthtech Landscape”.

“We’ve seen a surge of interest in Indonesia as an investment destination. We’ve seen a lot of activity in digital infrastructure, roads and other traditional infrastructure. It’s an exciting few years ahead.” - Nicola Yeomans, partner

The Omnibus Law: liberalising the economy, attracting investment

The Omnibus Law was officially enacted in November 2020 and represents one of the Indonesian government’s greatest efforts to accelerate economic growth. The objective of the measures is to liberalise the Indonesian economy and encourage foreign investment into Indonesia. Practically, it seeks to simplify processes for doing business in Indonesia to in turn grow the number and size of Indonesian businesses and create more employment opportunities for local and foreign workers.

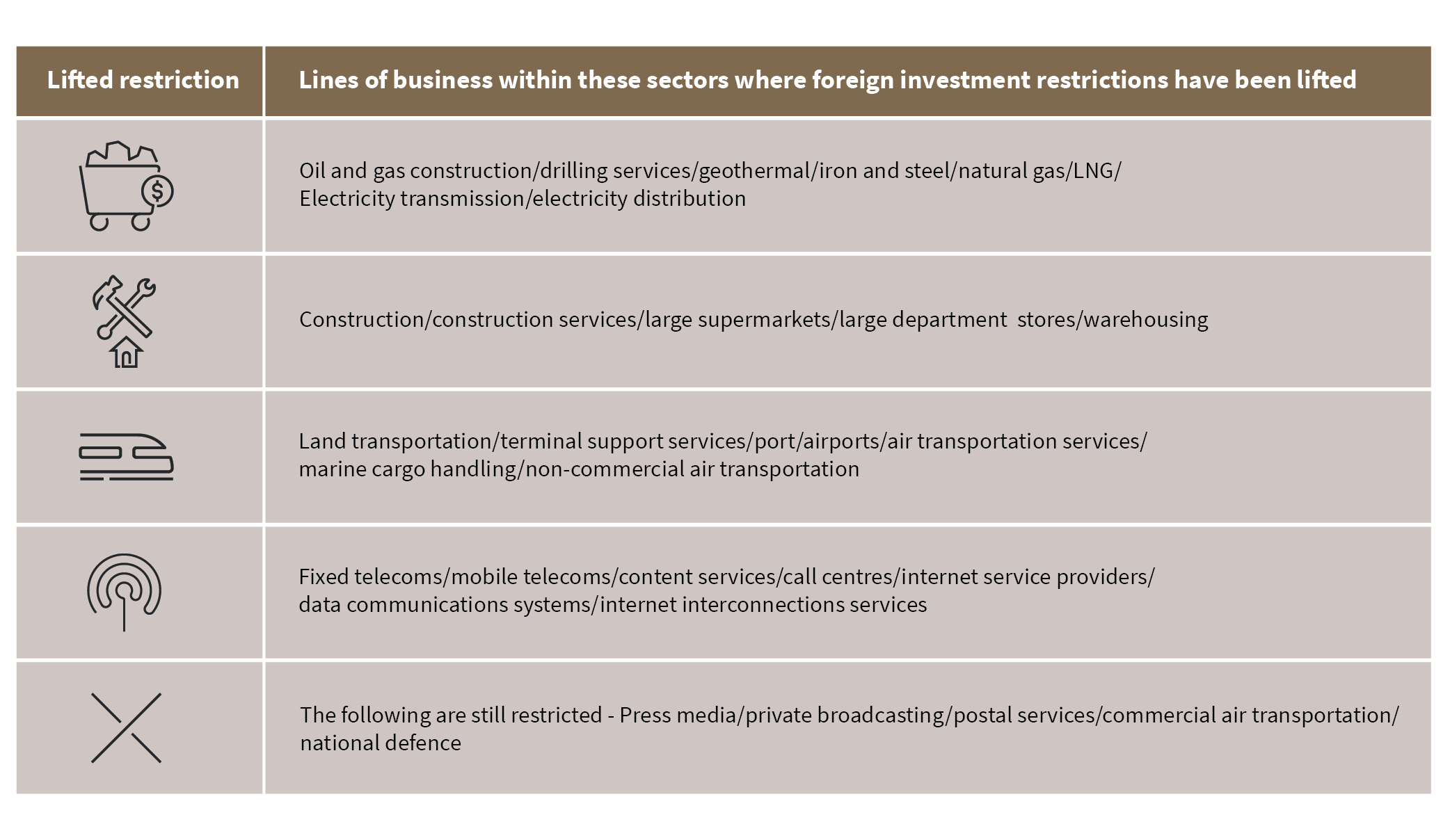

The Positive List: a dramatic shift in investment approach

Perhaps the largest change to accelerate economic growth is the introduction of the Positive List, replacing the previous Negative List, which limited foreign investment in most sectors. The key change in approach is that unless specified otherwise under the Omnibus Law, an Indonesian business can be 100% foreign owned.

The four notable areas now open to foreign ownership, which were previously restricted, are energy, construction, transportation and telecommunications. There are specific business lines within each of these areas (see the table below) in which specific rules apply under the Omnibus Law, however overall, the opening of these sectors for more foreign investment represents a dramatic shift to doing business in Indonesia.

Certain obvious areas remain restricted, being press media, private broadcasting, postal services, commercial air transportation and national defence.

The post-Covid restrictions investment surge

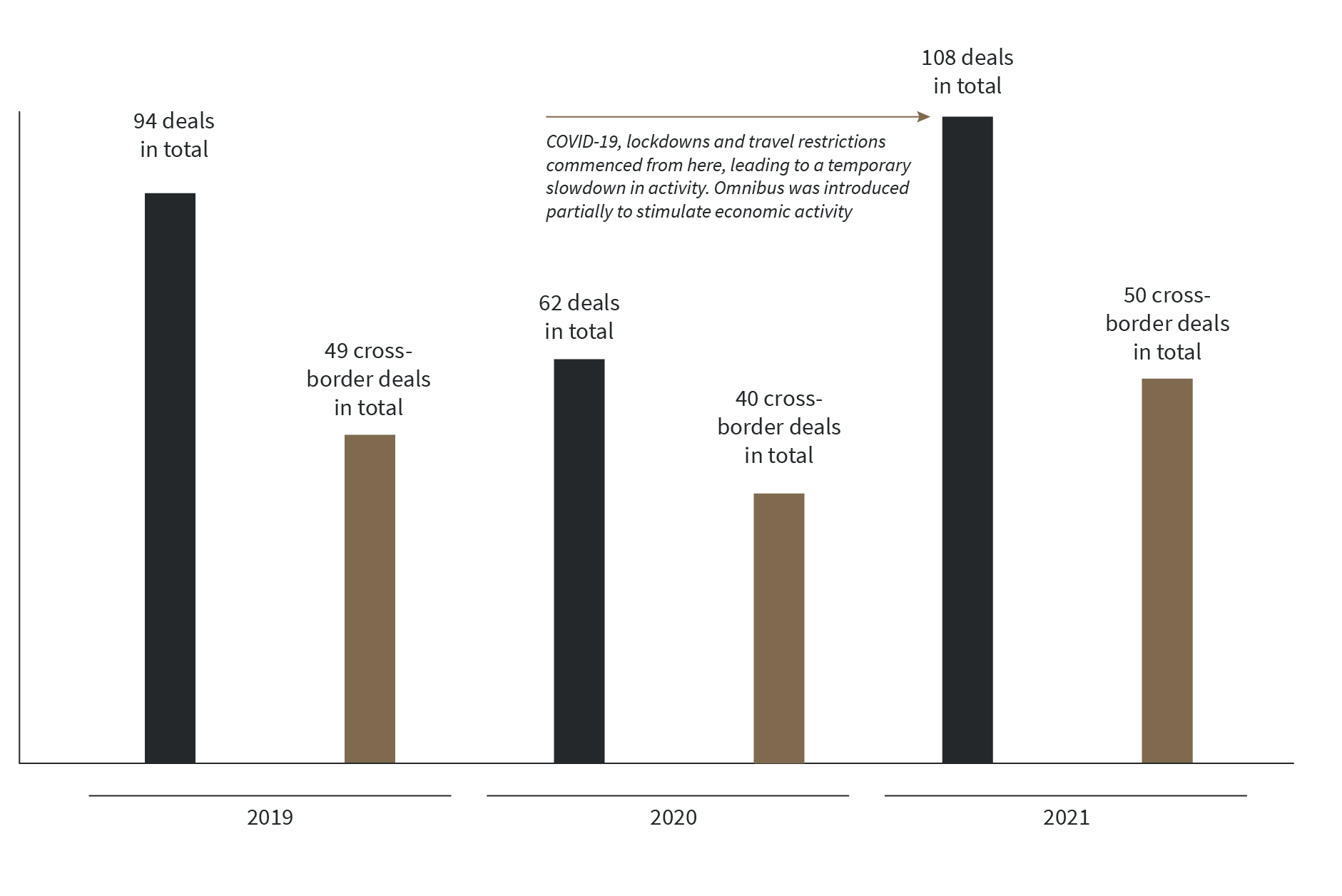

Indonesia experienced a sharp uptick in transaction activity, including cross-border transactions, in 2021, after a COVID-19 induced slowdown in 2020 (see chart below).[2] It is likely that the surge was driven by the opening of Indonesian businesses for foreign investment. Notable examples include Macquarie’s $610m investment into Bersama Digital Infrastructure and BDx’s $300m joint venture with Indosat Ooredoo Hutchison and Lintasarta, both of which King & Wood Mallesons acted for foreign investors involved in those transactions.

Mergermarket.

Indonesia’s new sovereign wealth fund – seeking $US20bn

Another momentous change introduced under the Omnibus Law is the creation of Indonesia’s sovereign wealth fund, the LPI. The LPI was seeded with government revenues but is designed to mainly be funded by third party investor commitments. Its focus is primarily on infrastructure projects and is open for third party investment to occur either through or alongside the LPI.[3] This structure closely follows that established by India by its sovereign infrastructure funds.

The LPI aims to attract US$20bn in third party investments. CDPQ, APG and ADIA have already signed a memorandum of understanding with the LPI committing, in aggregate, US$2.7bn to establish Indonesia’s first infrastructure investment platform.[4]

Other notable institutions that have committed in writing to fund projects through or alongside the LPI are GIC, IDFC, the Japan Bank for International Cooperation and the UAE Government.[5]

Governance of the LPI has been a key focus for foreign institutions committing to the LPI. Reputable and suitably qualified individuals have been carefully selected by the Widodo administration to ensure credibility of the LPI, with Ridha Wirakusumah (formerly of KKR, General Electric and Citi) being named its chief executive officer. It is intended for the Indonesian government to only be involved in the LPI in an advisory capacity, to ensure the LPI remains an independent body and maintains its transparency.

Tax reform – carbon trading towards a net zero economy

A spate of tax measures was also enacted under the Omnibus Law. Key aspects include the introduction of a carbon tax and a roadmap towards the introduction a carbon trading mechanism by 2025.

The carbon tax forms part of a broader push to transition Indonesia’s mining and energy sector towards the extraction of other resources (such as nickel) to strengthen export relationships with neighbouring nations housing the growing electric vehicle and battery manufacturing hubs, such as Malaysia. The push is also intended in the long-term to onshore electric vehicle and battery manufacturing in Indonesia.

The carbon trading roadmap forms part of Indonesia’s objective to achieve net zero emissions by 2060. This is in line with Indonesia’s commitments under the Paris Agreement, which it ratified in 2016.

Executing deals in Indonesia

With macro conditions making Indonesia an attractive destination for foreign investment, and a legal and regulatory environment designed to support such investment, foreign investors then need to turn their focus on how to execute deals in Indonesia to:

- conform to international business standards, and

- maintain a level of protection for the financial position and reputation of the foreign investor.

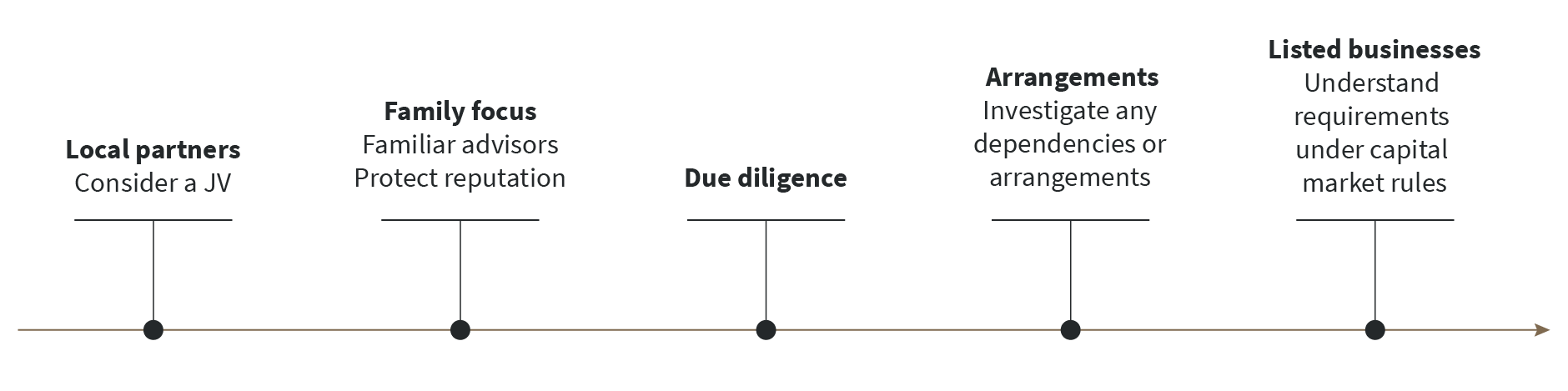

The local partner

Many investments into Indonesia are often structured as a joint venture with a local partner. Indonesia is a large and unique market and so in the short-term, the assistance of, and the alignment of interests with, a local joint venture partner can be crucial for success.

Keep in mind that many Indonesian businesses are also large family-owned businesses. Engagement of advisors that have experience in Indonesian transactions with a family business as the counterparty is crucial to properly manage this dynamic. Reputation is often a key concern for family businesses selling a stake. A foreign investor should also investigate any arrangements or dependencies which the business has with other parts of the family business, as such arrangements are unlikely to continue when the business is under the ownership or control of the foreign investor.

Special considerations may also apply where the local partner or its business is listed on the Indonesian stock exchange. The local partner or its business may be subject to certain requirements under Indonesia’s capital market rules that interact with specific provisions in a normal share purchase agreement or shareholders’ agreement, particularly in relation to share transfers. Again, engaging the right advisors with the relevant experience is crucial to navigate around these issues.

Contractual protections are no substitute for due diligence

This old saying comes into even sharper focus when executing deals in Indonesia. Ensure thorough due diligence of all types is completed so that a foreign investor is fully informed of any issues when negotiating the legal documentation for the transaction or even when deciding to proceed with the transaction at all.

Foreign investors should engage international and local counsels with the relevant experience of negotiating legal documentation that achieves the requisite level of contractual protections needed. Specifically, foreign investors should ensure strong protections are included for any known or prospective compliance issues identified as part of due diligence. Where the compliance issue is more pronounced, it may be that a clear walk away right is needed, with minimal financial and reputational damage for the foreign investor.

Governance

When transacting with local partners or businesses, it is important to quickly ascertain whether the partner or business is government linked. This may be easily identifiable where it is a State-owned enterprise. Where not so clear, attention should turn to an Indonesian company’s two-tiered board structure.

An Indonesian company has both a board of directors (who oversee the day-to-day operations of the company) and a board of commissioners (who oversee the board of directors and provide recommendations to it). Due diligence should be undertaken on the individuals sitting on these boards to ensure none of them are present members of government or closely government affiliated.

Going forward, a foreign investor’s “reserved matter” rights are crucial. “Reserved matters” are matters that a company may not carry out without the vote of either a certain shareholder or that shareholder’s nominated board member. A foreign investor should negotiate its reserved matter rights to ensure it has an ability to block any actions of a company where it relates to something that the investor deems important to the investor’s interests, whilst also not being intrusive to the day-to-day operations and growth of the company.

Particular considerations arise where an Indonesian business is listed on the Indonesian Stock Exchange, as certain reserved matters may be deemed “control” of the Indonesian company, triggering a requirement for that shareholder to conduct a mandatory tender offer to the other shareholders under Indonesia’s capital market rules.

With the right advice and careful consideration of the factors set out above, foreign investors can deploy their capital in a way that meets the criteria of all the various stakeholders involved.

The hunt for yield in Indonesia is fierce as foreign investors circle the opportunities.

“Other sectors attracting foreign interest are healthcare, fintech and digital payments.” - Azlan Mohamed Noh, senior associate