As the world transforms to net zero emissions and undergoes the most significant changes since the industrial revolution, the Federal Government’s decarbonisation plan aims to make Australia an indispensable part of the global economy.

The Federal Government’s Future Made in Australia plan, announced in the 2024-25 Federal Budget, is backed by a $22.7 billion investment over a decade. With legislation introduced into Parliament and the closure of the first round of consultations in respect of the Critical Minerals Production Tax Incentive (CMPTI) and the Hydrogen Production Tax Incentive (HPTI), we delve into the Future Made in Australia agenda.

What tax-related supports might best achieve the Future Made in Australia objectives? Do we also need tax-related policy changes outside the Future Made in Australia framework?

At least two things are clear: it is critical that the local and foreign investment community have more detail and clarity. And broader tax policy can – and should – play a central role in this transformation.

We are watching developments. Read on for more!

‘The Future Made in Australia plan is about attracting and enabling investment, making Australia a renewable energy superpower, value-adding to our resources and strengthening economic security, backing Australian ideas and investing in the people, communities and services that will drive our national success.’

- Prime Minister Anthony Albanese, 14 May 2024

- The Federal Government plans to invest $22.7 billion over a decade in the Future Made in Australia plan (plan) to help the country transition to a net zero emissions economy and become a key player in the global economy.

- The plan focuses on two streams: net zero transformation and economic resilience and security.

- The Future Made in Australia Bill 2024 was introduced into Parliament in July 2024 to establish criteria and processes for decision-making and provide certainty for private sector investment.

- The plan includes investments in renewable hydrogen, green metals, low carbon liquid fuels, critical minerals processing, and clean energy manufacturing.

- Community benefit principles will ensure investments benefit local communities, industries, supply chains and workers.

- There are unanswered questions regarding the eligibility requirements for two tax incentives introduced under the plan: the Critical Minerals Production Tax Incentive and the Hydrogen Production Tax Incentive.

- The Productivity Commission has raised concerns about the policy behind the plan and suggests holistic tax reform may be more effective.

- Additional tax-related supports may be necessary to achieve the goals of the plan, such as designated infrastructure project provisions and reviving the tax-exempt infrastructure borrowing concession.

- Recent changes to Australia's capital gains tax rules for foreign residents may impact decarbonisation projects and renewable energy investments in the country.

Background to A Future Made in Australia: attracting private capital, providing support

The Future Made in Australia agenda will help Australia build a stronger, more diversified and more resilient economy powered by renewable energy, create more secure, well‑paid jobs and encourage and facilitate the private sector investment required to make the most of this structural shift.

Which sectors are chosen?

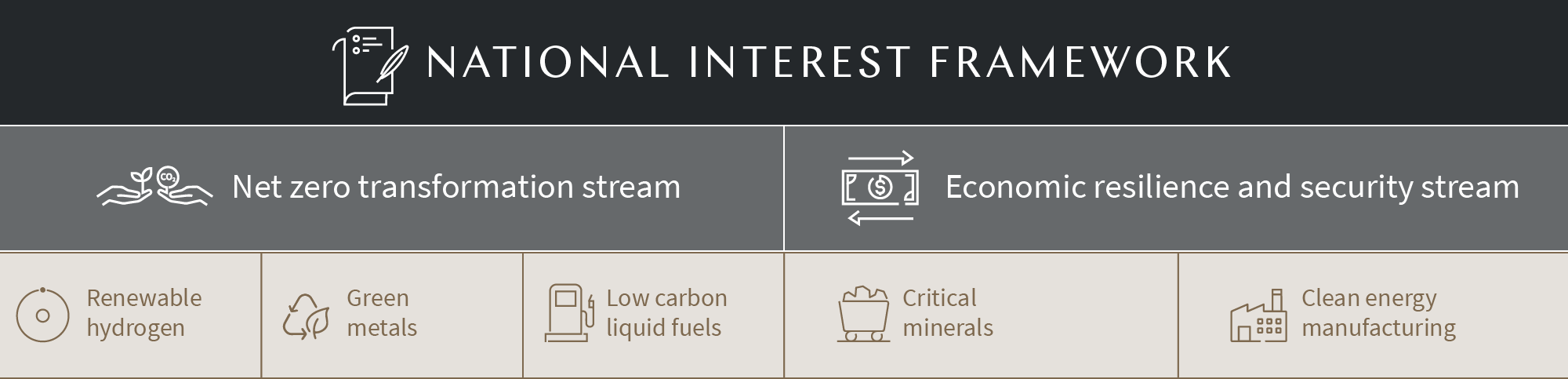

The policy focuses on two streams: the ‘net zero transformation stream’ and the ‘economic resilience and security stream’. These sit within a National Interest Framework, contained in the Future Made in Australia Bill 2024 (Bill) introduced into Federal Parliament on 3 July 2024.

The supporting paper for the 2024-25 Budget National Interest Framework identified how assessments against the framework informed policy decisions:

- Government investments in line with the net zero transformation stream of the framework focused on renewable hydrogen, green metals and low carbon liquid fuels.

- Government investments aligned with the economic security and resilience stream focussed on refining and processing critical minerals and clean energy manufacturing.

The Bill seeks to establish criteria and processes for decision-making and provide certainty for the private sector to attract private capital in areas of national interest, by establishing:

- a National Interest Framework to support the consideration of, and decision-making in relation to, significant public investment that unlocks private investment at scale in the national interest

- an assessment process to identify opportunities in sectors of the Australian economy that align with the National Interest Framework, being sectors where:

- Australia could have a sustained comparative advantage in a net zero global economy and public investment is likely to be needed for the sector to make a significant contribution to emissions reduction at an efficient cost (the net zero transformation stream), or

- some level of domestic capability is a necessary or efficient way to deliver economic resilience and security, and the private sector will not deliver the necessary investment in the sector in the absence of government support (the economic resilience and security stream), and

- community benefit principles that must be considered by decision-makers in determining whether Future Made in Australia support should be provided.

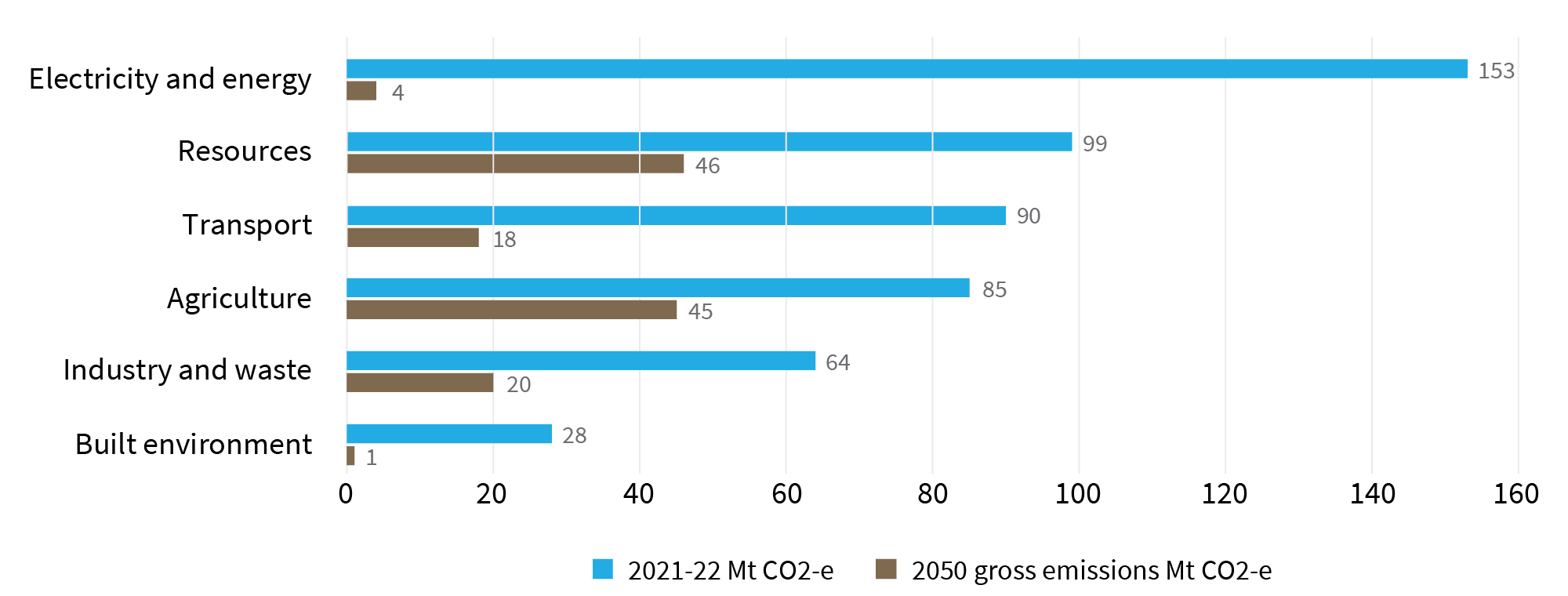

The Climate Change Authority, at the request of the Australian Parliament, undertook a review of the potential technology transition and emission pathways that best support Australia’s transition to net zero emissions by 2050. In its report released in September 2024 it identifies six sectors – electricity and energy, transport, industry and waste, agriculture and land, resources and the built environment. The planned emissions reductions of these six sectors compared to current emissions are set out below.

Source: The Climate Change Authority, Sector Pathways Review

The transition to net zero involves more than each sector moving along technology-based decarbonisation pathways. It requires actively managing a major reorganisation of public and private finance, supply chains, production systems, industrial zones, energy sources, infrastructure and workforces within Australia. It also involves overcoming the barriers that the Climate Change Authority has identified as standing in the way of achieving net zero by 2050. The tax system will likely have a significant role to play in this transition and in overcoming these barriers.

‘A review of the Australian tax and transfer system could potentially reveal opportunities to reallocate public funding to better align with the government’s Net Zero Plan.’

- The Climate Change Authority, Sector Pathways Review

What support is proposed?

The Bill establishes broad parameters around Future Made in Australia support. Such support may include a grant, loan, indemnity, guarantee, warranty, investment of money or equity investment that is:

- provided under the Future Made in Australia Innovation Fund or by the Export Finance Insurance Corporation;

- identified as Future Made in Australia support under another Commonwealth law; or

- prescribed by the rules for this purpose.

How will it evolve over time?

Under the Bill, the Minister has powers to make rules in relation to the provision of Future Made in Australia support. These include rules prescribing requirements that must be complied with, methods or criteria that must be applied, or matters that may, must or must not be taken into account in applying for support, deciding whether support should be provided, or providing support.

A sector assessment must consider such of the following matters as the Secretary considers relevant to the conduct of the assessment:

- whether Australia could be competitive in the sector;

- whether the sector could contribute to an orderly path to net zero transformation, including through the use of renewable energy;

- whether the sector could build the capabilities of the Australian people and the regions of Australia, and generate employment opportunities;

- whether support for the sector could improve Australia’s economic resilience and security;

- whether support for the sector could:

- recognise the key role of the private sector; and

- deliver genuine value for money.

The Future Made in Australia package includes support for investment in critical minerals processing and hydrogen production as industries aligned with the National Interest Framework. Details of the critical minerals aspects of the package are here and here. This package includes the CMPTI, valued at $7 billion. The CMPTI is the largest initiative within the package, which also includes funding to map Australia’s resource endowments to identify potential discoveries of all critical minerals. Our thoughts on the CMPTI, based on the consultation paper released on 28 June 2024, are here.

The Bill itself does not set out the process for how Future Made in Australia support will be provided, and allows the Minister to make rules relating to the application for and provision of the support, decisions about whether Future Made in Australia support should be provided, and methods, criteria or other matters that may, must, or must not, be taken into account in this respect.

How will the community benefit principles work?

Decision-makers will apply a set of community benefit principles to encourage investment in local communities, domestic industries, supply chains and skills, and promote diverse workforces, secure jobs and tax law compliance. These will apply for each Future Made in Australia support and will be enforced appropriately. This includes through Future Made in Australia plans, which certain recipients of Future Made in Australia support will be required to have.

The community benefit principles are to:

- promote safe and secure jobs that are well paid and have good conditions

- develop more skilled and inclusive workforces, including by investing in training and skills development and broadening opportunities for workforce participation

- engage collaboratively with and achieve positive outcomes for local communities, such as First Nations communities and communities directly affected by the transition to net zero

- strengthen domestic industrial capabilities including through stronger local supply chains, and

- demonstrate transparency and compliance in relation to the management of tax affairs, including benefits received under Future Made in Australia

The Minister may specify additional community benefit principles through rules.

How the tax incentives for critical minerals and hydrogen work - the two supports already announced (CMPTI and HPTI)

Two Future Made in Australia supports announced in the 2024-25 Federal Budget were the CMPTI and the HPTI.

The first round of consultation in respect of the CMPTI and the HPTI closed on 12 July 2024. The discussion in the respective consultation papers is a useful starting point in understanding the scope of the incentives. Amongst other things, detail is provided as to how the CMPTI and the HPTI will be delivered through Australia’s tax system as a refundable tax offset (with the ability for entities to also adjust their Pay As You Go instalment rate based on the expected credit where they are in a tax payable position).

- The CMPTI will be available at a rate of 10 per cent of eligible processing expenditure incurred by an eligible entity.

- The HPTI will be available at a rate of $2 per kilogram of eligible hydrogen produced.

As we set out here, for now much of the detail regarding the eligibility requirements of the CMPTI has not been provided. This includes broader eligibility requirements that align with the Future Made in Australia community benefit principles. Similar observations can be made in respect of the HPTI.

Structural questions and issues with the CMPTI and the HPTI

There are a number of unanswered questions in respect of the community benefit principles in the context of the CMPTI and the HPTI. At a high level, these relate to how, and when, entities wanting to receive the incentive must satisfy the community benefit principles.

Currently, the explanatory memorandum to the Bill provides only that:

[t]he requirement for decision makers to have regard to Community Benefit Principles can be satisfied through further specification of requirements for Future Made in Australia supports on a program-by-program basis, such as by issuing guidance in a Statement of Expectations to an independent authority, implementing specific requirements as part of relevant legislation or program guidelines, or requiring the satisfaction of a Future Made in Australia Plan.

We set out here the matters that will be important in respect of the CMPTI, and whether some of the design features contained in the consultation paper will impact the effectiveness of the CMPTI as a support that will help achieve economic resilience and security (by incentivising downstream processing of critical minerals in Australia). These matters and issues are equally applicable in respect of the HPTI, including whether it will help achieve net zero transformation because the renewably hydrogen sector has a sustained comparative advantage in a net zero global economy.

There may be some challenges with linking the community benefit principles to tax measures such as the CMPTI and the HPTI.

- There is a question as to whether the incentives will achieve their intended purpose in the absence of certainty about the application of the community benefit principles and other related matters. Submissions made to the Senate Economics Legislation Committee regarding the Bill and the Future Made in Australia (Omnibus Amendments No. 1) Bill 2024 (as set out in the Committee’s report dated 6 September 2024) expressed similar concerns about the community benefit principles (eg the need for them to be objective and clear to provide certainty for taxpayers to at least initially self-assess eligibility for final investment decision deliberations).

- There are broader economy wide issues that the critical minerals and renewable hydrogen industries are experiencing. For example, despite saying that the Federal Labor government should push ahead with tax incentives for green-hydrogen producers (such as the HPTI and the Hydrogen Headstart program), Fortescue recently announced that it was abandoning its 2030 target for green hydrogen production and that it would pivot its clean energy ambitions to refocus on generating renewable electricity.

Are additional tax-related supports necessary? Some say a strong ‘yes’

The Productivity Commission and others have raised concerns about the policy behind Future Made in Australia. For example, it has been argued that holistic tax reform that would boost the incentive for investment and work in more productive activities would be preferable to incentives through the tax system, as would be the case with the CMPTI and the HPTI and the model of providing refundable tax offsets.

‘They are not tax reform, they are a tax policy.’

- Productivity Commission chairwoman Danielle Wood, quoted in The AFR, 4 June 2024

Against this backdrop, what else could be done from a tax perspective to meet the Future Made in Australia agenda of attracting investment and making Australia a renewable energy superpower?

The climate change measures we’re missing

Australia’s income tax legislation contains a Part headed ‘climate change’, enacted in 2011. At that time, provisions regarding registered emissions units – Kyoto units and, more relevantly, Australian carbon credit units – were introduced. Those provisions provide clarity as to the tax treatment of registered emissions units where such clarity might not otherwise have existed.

While helpful, they don’t address climate change and decarbonisation – they are not tax-incentive style provisions. And they don’t address all credits generated by decarbonisation projects. For example, they don’t address large-scale generation certificates (created in respect of electricity generated from a power station's renewable energy sources) or Safeguard Mechanism credit units.

Thirteen years later, those provisions remain the only provisions in the Part. There is a lack of specific climate change-related tax measures, particularly at a corporate tax level.

What we do have: Current tax-related supports

Aside from the registered emissions units’ provisions, there is a hierarchy of provisions to consider when assessing the tax profile – and specifically – deductibility, of decarbonisation related expenditure. The following are of most relevance:

- A deduction (over a period of about 14 years) for amounts of capital expenditure incurred on establishing trees in a carbon sink forests where, amongst other things:

- the primary and principal purpose of the entity incurring the expenditure for establishing the trees is carbon sequestration by the trees; and

- the establishing entity’s purposes for establishing the trees do not include felling the trees or using them for commercial horticulture.

- A deduction for capital expenditure that forms part of the cost of a depreciating asset. The deduction is spread over the effective life of the depreciating asset.

- ‘Project pool rules’ allow a deduction over the life of a project for certain expenditure associated with projects carried on by taxpayers that are allocated to a project pool. This includes an amount of capital expenditure incurred:

- to undertake feasibility studies for a project;

- for environmental assessments for the project; or

- to obtain information associated with a project,

so far as it is directly connected with a project carried on, or proposed to be carried on, for a taxable purpose (which is broader than just deriving assessable income – for example, it includes environmental protection activities).

- An immediate deduction for expenditure incurred for the sole or dominant purpose of carrying on ‘environmental protection activities’ (eg activities undertaken to prevent, fight or remedy pollution resulting, or likely to result, from your earning activity; and treating, cleaning up, removing or storing waste resulting, or likely to result, from your earning activity). Such activities can include geological sequestration activities.

- Certain business-related capital expenditure (referred to as “black hole” expenditure) is deductible over five years, if:

- the expenditure is not otherwise taken into account;

- a deduction is not denied by some other provision;

- the business is, was or is proposed to be carried on for a taxable purpose; and

- a limitation does not apply to preclude deductibility.

What we could have: Further tax-related supports?

So what else can we do tax reform wise to encourage the activities that we need to undertake to meet our net zero targets?

The overarching theme in respect of tax-related decarbonisation-specific reform measures is what type of activity do we want to encourage – and how, from a tax perspective, do we provide an incentive to engage in it. Broadly, the aim is to decarbonise and to electrify using renewable sources of energy. The tax levers that can be pulled include:

- providing specific deductions where they might not otherwise be available;

- providing accelerated, or enhanced deductions (eg instant asset tax write-offs, or deductions equal to 150% of the asset’s cost), where deductions are currently available;

- concessions regarding the utilisation of tax losses (eg to make it easier to satisfy the continuity of ownership test (COT) or same/similar business test (SBT) – or to dispense with one or more of these tests in respect of losses from decarbonisation expenditure)

- specific tax offsets generated by particular activities (eg the CMPTI and the HPTI).

Three possible options are discussed below.

Option: Designated infrastructure project provisions

Division 415 of the Income Tax Assessment Act 1997 provides for special treatment for tax losses and bad debts for certain entities (called ‘designated infrastructure project entities’) that carry on infrastructure projects that the Infrastructure CEO designates under the provisions.

More specifically, it allows companies and fixed trusts that are carried on exclusively for the purpose of a ‘designated infrastructure project’ to uplift the value of tax losses from earlier years by the long-term bond rate. The provisions also exempt companies from the COT and SBT and exempt fixed trusts from the trust loss and bad debt deduction tests.

When introduced in 2013, the relevant explanatory memorandum noted that investment in high quality infrastructure projects was critical to improving national productivity and underpinning economic growth. Similarly, investment in decarbonisation and electrification projects are critical to Australia meeting its emission reduction targets.

It was noted that infrastructure projects often experience long lead times between incurring deductible expenditure in the construction phase and earning assessable income in the operational phase. Tax losses are therefore accumulated and carried forward to later income years awaiting the receipt of income. As such, the present value of losses may be eroded over time, disadvantaging infrastructure investment compared to other types of investment. Furthermore, infrastructure projects may move through a number of phases as they move from the construction phase to the operational phase, and the entity may have different owners as it moves through its different phases. These changes could result in the entity no longer being able to use its tax losses to offset against future income, eroding the value of the losses altogether. These challenges and issues are, to varying degrees, equally applicable for decarbonisation and electrification projects.

Therefore, the measure encourages private investment in nationally significant infrastructure projects by:

- ensuring that investors are not discouraged from investing in infrastructure because of the reduction in the present value of losses over time, and

- increasing the likelihood that the losses can be used to offset future earnings and benefit investors in the project, whether the original investors or new investors in the project.

These same concerns could present themselves in respect of decarbonisation projects.

Therefore, while there is a question as to what modifications would, or might, be required in the context of nationally-significant decarbonisation projects, Division 415 could be used (or its application modified so that it was clear it could be used) for in respect of applicable climate-related activities.

Option: Reviving the former tax exempt infrastructure borrowing concession

Former Division 16L of Part III of the Income Tax Assessment Act 1936, together with related legislation, established the tax exempt infrastructure borrowing concession. This concession provided for income in relation to borrowings for certain infrastructure projects to be non-assessable, but also not to give rise to deductions, for a 15 year period, subject to conditions being met in relation to the project and the use of the borrowings (eg the identity and ownership of the borrowing entity, the spending of borrowed money and the nature and use of facilities on which moneys are spent).

The tax exempt infrastructure borrowing concession was closed to new projects in 1997. It is understood that the incentives may have been withdrawn due to aggressive financing arrangements that, in the view of the government, were directed more at tax avoidance than infrastructure construction.

When operative, the purpose of the provisions was to facilitate private investment in the construction of certain public infrastructure projects by enabling owner-developers of such projects to obtain tax-exempt or tax-rebatable financing. In allowing the incentives, the government recognised that owner-developers may be in a tax loss position, and therefore be unable to benefit from tax deductions for interest costs incurred. The provisions effectively enabled the owner-developer to transfer the interest deduction incurred on borrowings to the providers of the finance (thus interest on infrastructure borrowings was non-deductible to the borrower for up to 15 years). In turn, this resulted in the borrower obtaining lower interest rates. It was likewise broadly non-assessable to the lender for the same period.

There were three categories of infrastructure borrowings:

- Direct infrastructure borrowing (ie borrowing by a company to spend on constructing an infrastructure facility and/or related facilities which it intended to own, sell or use before sale in prescribed circumstances).

- Indirect infrastructure borrowing (ie borrowing by a company to lend to another person for whom the borrowing will be a direct infrastructure borrowing).

- Refinancing infrastructure borrowing (ie borrowing to refinance a direct or indirect infrastructure borrowing or previous refinancing infrastructure borrowing).

The borrower of direct infrastructure borrowings must, at the time of borrowing, have intended to spend the borrowed amounts only on one or more of seven specified kinds of “infrastructure facilities”, and/or on “related facilities”. The seven basic kinds of infrastructure facility were:

- land transport

- air transport

- seaport

- electricity generation, transmission or distribution

- gas pipeline

- water supply, and

- sewerage or waste water.

So, could a form of the former tax-exempt infrastructure borrowing provisions be used to encourage decarbonisation-related project borrowings? The framework seems to have been in place – for example, spending of borrowed money on particular types of facilities such as electricity generation (eg wind or solar farms and hydrogen production), which could be tailored to include other decarbonisation activities such as carbon capture and storage. With similar safeguards to those under the designated infrastructure project provisions – plus others to ensure the renewed provisions operated as intended - or a form of community benefit principles such as under Future Made in Australia, such an option should not be ruled out.

Option: Modified or replicated Division 40 provisions

Many of the current tax-related supports in could also be modified, or replicated, to provide deductions for decarbonisation / electrification related activities (to the extent that they don’t already apply). For example, feasibility related to such activities could be expressly made immediately deductible, in case there was any doubt that a deduction was not available under existing provisions.

And what impact will the recent announcements to capital gains tax for foreign residents have on decarbonisation and Australia’s net zero target?

At the same time as announcing the Future Made in Australia plan, the Federal Government announced changes to Australia’s capital gains tax (CGT) rules as they apply to foreign residents that have the potential to fundamentally alter the decarbonisation project landscape in Australia.

Further detail on these changes are contained in a consultation paper, ‘Strengthening the foreign resident capital gains tax regime’ (Consultation Paper). These changes will have significant implications for non-residents and are being introduced without any transitional relief.

- They will apply to CGT events which occur on or after 1 July 2025, including in respect of investments made prior to that date.

- As such, non-residents who may have invested, or are considering investing, into Australian assets, including renewable projects, on the basis that they would not have been subject to Australian tax on exit will now need to factor Australian tax into their modelling.

In summary, the Federal Government considers that under the current law, there is uncertainty for Australian income tax purposes as to which assets should be treated as real property when applying the foreign resident CGT regime. This is because there is no statutory definition of ‘real property’ and its scope and meaning have been the subject of much conjecture, including, in particular, whether certain assets, such as wind turbines, are fixtures and, as such, are ‘real property’.

To address these issues, certain assets that are considered to have a ‘close economic connection to Australian land and/or natural resources’ are now proposed to be treated in the same way as existing ‘taxable Australian real property’. They will include:

- infrastructure and machinery installed on land situated in Australia, including land subject to a mining, quarrying or prospecting right of an entity. For example:

- energy and telecommunications infrastructure, such as wind turbines, solar panels, batteries, transmission towers, transmission lines and substations;

- transport infrastructure, such as rail networks, ports and airports;

- heavy machinery installed on land for use in mining operations, such as mining drills and ore crushers;

- a non-portfolio membership interest in an entity where more than 50% of the underlying entity's market value is derived from the above assets.

Our more detailed comments on the Consultation Paper are here.

What is next? Watch this space

The Future Made in Australia framework and agenda, and supports such as the CMPTI and the HPTI, provide a solid platform from which Australia can move to achieve its net zero targets. However, as we highlight above, there are some concerns about whether this will be enough. And the announced changes to Australia’s CGT rules as they apply to foreign residents have the potential to significantly impact the renewable energy investment landscape in Australia. Clear signalling to the local and foreign investment community is critical in this regard. Broader tax policy can – and should – play a central role in this transformation.

Want to know more? See our related insights:

Interested in our insights and experience on the future of energy including hydrogen, offshore wind and energy regulation?