When China’s national carbon market launched in 2021, it promised to act as a powerful tool in combatting climate change. The whirlwind year that followed saw total trading volume reach 200 million tonnes and new environmental information reporting requirements introduced.

- China’s national carbon markets are expected to expand to sectors beyond power, such as iron, steel and aviation

- China’s regional markets have already expanded, such as Guangdong’s scheme adding data centres in 2022

- A shift is under way, from free allocation of carbon allowances to an auction system

- There are positive signs for a possible relaunch of emission certificates (China Certified Emission Reduction)

- Major polluters (among others) face new requirements for detailed environmental information in annual reports

- The first cross-border carbon trade has happened.

Now, as we enter the Year of the Rabbit, the world’s largest carbon market, covering more than 4 billion tonnes of power sector CO2, is expected to expand into new sectors beyond power generation. There is no clear time expectation, but the trend of the expansion is clear. In late 2022, companies from industries beyond power generation were brought into the national regime. They have no mandatory offset obligations, only reporting duties.

We anticipate another year of strong growth for China’s carbon markets, both national and pre-existing regional markets, as well as cross-border trade.

In this insight, as part of our ongoing series exploring carbon markets, we give an overview of the critical shifts within China’s carbon markets in 2022 and how they inform what’s to come in 2023.

To understand how China’s national carbon market operates, see our featured insight on Trading Carbon in China.

To sharpen your edge and stay up to date in the carbon markets space, subscribe to our Climate & ESG insights here.

Regional markets are expanding, and the national market will follow

China’s national and regional carbon markets are expanding to sectors beyond power generation. It is hoped that this expansion will bring more market participants, increase trade volume and stabilise the market.

National Carbon Market

China’s national carbon market currently covers the power sector, capturing more than 2,000 entities labelled the “Emission-controlled Enterprises”. Given the success of the first compliance cycle in late 2021, the national carbon market is set to progressively expand to other energy-intensive sectors. This includes petrochemicals, chemicals, building materials, iron and steel, non-ferrous metals, papermaking and domestic aviation.

In late September 2022, the Beijing Municipal Ecology and Environment Bureau added companies from industries other than the power generation industry to the national carbon market. However, these companies are regarded as “reporting entities” instead of “compliance entities”, meaning they only have a reporting duty. They face no mandatory obligation to offset their emissions.

On 3 January 2023, an official from the Ministry of Ecology and Environment stated that China will expand the national market to other industries gradually, while maintaining the good operation of the quota spot market of the power generation industry.

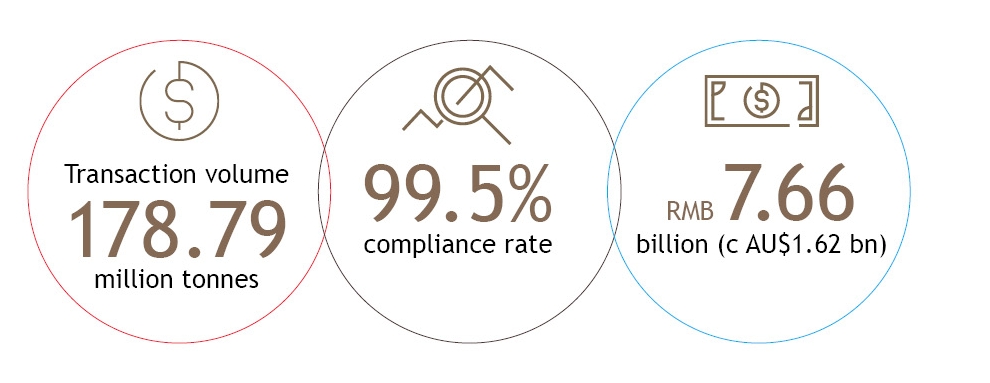

Success of the first compliance cycle (114 days) in late 2022: Chinese Emission Allowance (CEA) transactions

Source: Carbon Neutrality journal, accessed via SpringerLink

Regional Carbon Markets

Regional markets pre-date the national market and have continued in parallel (albeit entities covered by the national scheme are exempted from regional schemes). Expansions in 2022 included:

Shanghai

An additional 16 entities were added to the ambit of the Shanghai carbon market in early 2022. This brought the total number of Emission Controlled Enterprises to 321. The additional 16 entities belong to a range of sectors including food manufacturing, pharmaceutical, car manufacturing and technology.

Guangdong

The Guangdong province trading scheme initially covered the power, iron and steel, cement and petrochemical sectors. Operational since 2013, the Guangdong carbon market has progressively expanded to include:

- aviation and papermaking in 2016

- ceramics, textiles and data centres in 2022.

Shift away from free allocation towards auctions

The Chinese government has indicated that the national carbon market will transition away from the free allocation of CEAs towards an auctioning system in line with the 30∙60 Target (peak emissions by 2030, carbon neutrality by 2060).

The Shanghai regional carbon market has gone a step further and currently facilitates the occasional auction of allowances.

This shift away from free allocation is important because:

- auctions raise the cost of allowances, making it more expensive to emit greenhouse gasses (GHGs) and therefore incentivising enterprises to reduce emissions

- the introduction of partial auctioning is expected to diversify decarbonisation solutions in China by not only encouraging additional renewables and CCUS deployment but also via improvements in gas generation and coal fleet efficiency.

The auctions involve a straightforward and transparent bidding process.

- A government body such as the Shanghai Ecological Environment Bureau will issue the announcement regarding auction of the carbon emission allowance.

- Qualified participants must complete the operation on the designated platform according to instructions.

The expected return of the CCER (China Certified Emission Reduction)

The CCER scheme came to a halt in 2017. Entities participating in the national carbon market can currently offset 5% of their verified emissions through the purchase of pre-existing CCERs.

There is no official announced timeline for the relaunch of the national CCER. In the past year, regulators have given positive signals. For example, the Ministry of Ecology and Environment head of climate change office Li Gao told the International Finance Forum (IFF) on 4 December 2022 that China will endeavour to further improve the CCER trading mechanism and relaunch the CCER trading market as soon as possible.

There is speculation that the Chinese government will permit the trading of newly generated CCERs.

The inclusion of newly generated CCERs would greatly expand eligible market participants. Currently only CEAs are tradable. Given that CEAs are only afforded to Emission Controlled Enterprises, all other companies are precluded from participating in the national carbon market.

The reintroduction of CCERs would address this by introducing a tradable asset to companies that abate GHG emissions such as renewable energy providers. These companies could sell their CCERs to Emission-Controlled Enterprises wanting to offset their verified emissions. Extra revenue from CCERs may incentivise more enterprises to actively reduce emissions.

For more information on CCERs see our insight on China’s carbon markets as a key tool to achieve net zero.

Increased disclosure requirement

In early 2022 new measures came into force which standardise and mandate ESG reporting.

The Administrative Measures for the Legal Disclosure of Enterprise Environmental Information require companies with a high environmental impact to submit annual reports. This includes companies that are major polluters as well as any publicly listed and bond issuing companies recently penalised for ecological or environmental violations.

The annual report must detail environmental information for the previous 12 months by March 15 of each year. At a minimum this must cover:

- basic company information, including information on company production and environmental protection

- environmental management, including ecological and environmental administrative licenses environmental protection tax, environmental pollution liability insurance, and environmental protection credit evaluation

- production, management and discharge of pollutants, including pollution prevention facilities, pollution emissions, discharge of toxic and hazardous matter, and the production, storage, flow, utilisation, handling, and self-monitoring of industrial solid and hazardous waste

- carbon emissions, including on the volume of emissions and emissions facilities

- ecological and environmental emergency response mechanisms, including information on emergency plans for environmental crises or disasters and emergency responses to heavily polluted weather

- environmental violations

- any other ad hoc environmental information legally required to be disclosed, and

- any other environmental information stipulated by laws and regulations.

Companies that fail to disclose or disclose incorrect information could be liable for penalties between RMB 10,000 (around AU$2,100) to RMB 100,000 (around AU$$21,000).

What next?

The Year of the Tiger gave China’s national carbon market the opportunity to settle into place and grow. We are closely watching developments as the carbon markets evolve in The Year of the Rabbit.

We consider that the focus of China’s carbon market in 2023 will remain the expansion of both national and regional markets, and the possible resurrection of the CCER.

Meanwhile, cross-border carbon trade also deserves our attention. China’s first cross-border carbon trade was completed in the Hainan International Carbon Emissions Exchange on 30 December 2022. The establishment of Core Climate by HKEX may further encourage China to connect its national carbon market to international carbon market.

For more information…

…on China’s carbon markets, see our insight on Carbon Markets in China.

…on the opportunities for China and Australia to collaborate towards a net zero economy, see our Pulse blog post on the launch of the ACBC-KWM Climate Collaboration Report.

Thank you to Eliza Saville for drafting assistance.

Stay up to date with our Carbon Market series, where we share our insights on a complex and evolving landscape, by subscribing here.