The long-awaited renewal of the China Certified Emission Reductions (CCER) market is expected to drive trading activity, develop the market and spur innovation. This is a critical step towards China reaching its ‘30.60’ decarbonisation target: peak emissions by 2030 and carbon neutrality by 2060.

In this three-part series, Shanghai-based KWM partner Molly Su and her team of specialists explain the change and its implications.

In this, the first insight, we look at the voluntary scheme - old and renewed. What does it involve and how is it different to the original market introduced in 2012? What does it mean for international investors and cross-border trading opportunities? What does this mean for the development of Hong Kong as a carbon trading hub capable of facilitating access for international investors to onshore CCERs and mobilising offshore capital to help China achieve its transition targets? How will it invigorate financial tools and derivatives? And why do we think it will lead to a more mature and dynamic trading market?

Need help? Reach out to Molly Su or your KWM contact

- China’s voluntary carbon market is based on issuing and trading CCER

- The CCER was introduced in 2012, but registrations were suspended in 2017 – and trading activity declined

- The Ministry of Ecology and Environment has prepared new infrastructure and regulations to restart the voluntary scheme

- We expect the new scheme will significantly boost trading activity and encourage new financial tools and derivatives in the market

- We are watching developments in cross-border trade and opportunities

Opening trading to more businesses: the voluntary carbon market potential

China’s Voluntary Carbon Market (VCM) is centred on the issuance and trade of CCER. The involvement of businesses and individuals in the carbon market is mainly through VCM participation, rather than the compulsory scheme.

In contrast to the Compliance Carbon Market (CCM), the primary participants in the VCM are businesses or individuals that voluntarily buy carbon credits to offset their own carbon emissions rather than those who are legally obligated to mandatory emission reductions. Currently, the national CCM – the National Emissions Trading Scheme (National ETS) - captures a little more than 2,000 entities from the power generation industry. Other businesses and individuals have limited opportunities for participation in the CCM.

Yet the national ETS and VCM are not entirely independent: CCM participants can offset a small portion of emissions using credits from the VCM. Under the Measures for the Administration of Carbon Emissions Trading (for Trial Implementation), key emitting entities may offset the settlement of carbon emission allowances (CEA) with CCER every year, up to a limit of 5%.

The voluntary scheme – a short history

|

June 2012

|

CCER scheme launched by the National Development and Reform Commission (NDRC), under the Interim Measures for the Administration of Voluntary Emission Reduction Transactions of Greenhouse Gases (Interim Measures). |

|

|

|

2015

|

Voluntary Emission Reduction Trading Information Platform launches Official trading of CCER commences |

|

|

|

2017

|

Trading restricted to a small number of existing registered entities, after NDRC suspends registration under Announcement No. 2 of 2017 on March 14

|

|

|

|

2017- January 2024

|

Trading activity within the CCER market enters period of decline Potential participants maintain interest in the scheme restarting |

|

|

|

2018

|

Ministry of Ecology and Environment (MEE) formally established under The Institutional Reform Plan of the State Council, adopted by National People's Congress on March 18, 2018

|

|

|

A new phase emerges: hitting ‘fast-forward’ to renew CCER

Throughout 2023, several indications revealed efforts to restart the CCER scheme within the year - including preparing trading infrastructure and advancing the legislative process. This hit the "fast-forward" button for a CCER restart.

- In March 2023, the MEE started to publicly request suggestions for CCER projects methodologies

- In May 2023, China Beijing Green Exchange finished the public procurement of technical services and the functional and performance tests of the CCER trading system

- On May 30, 2023, Li Gao, the head of the Climate Change Department of the MEE and a member of the National People's Congress Environmental Affairs Committee, informed reporters at the Zhongguancun Forum Forest and Grass Carbon Sinks Innovation International Forum that efforts were underway to restart the CCER scheme that year and to establish a unified national CCER trading system

- On October 19, 2023, the MEE, in conjunction with the State Administration for Market Regulation (SAMR), unveiled the eagerly anticipated Measures for the Administration of Voluntary Reduction of Greenhouse Gas Emissions and Emissions Credits Trading (For Trial Implementation) (Administrative Measures).

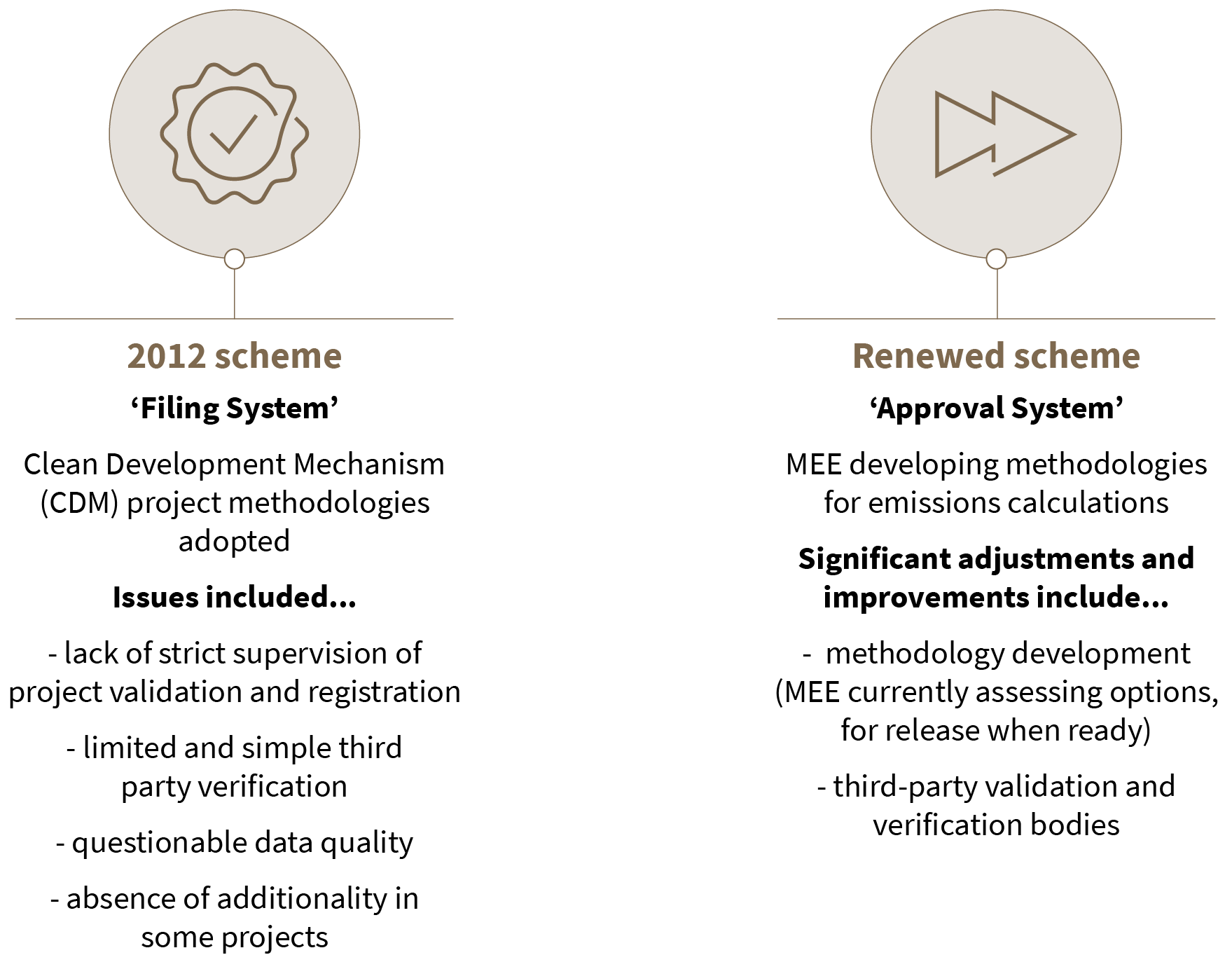

How will the new scheme work? Key points and major changes of Administrative Measures

Which projects can apply for CCER?

All projects applying for CCER should essentially fall under “emission reduction”. There are logically two ways to reduce emissions:

- Carbon mitigation: reduce existing GHG emissions

- Carbon sequestration: increase the absorption and removal of GHG

The need for Authenticity, Uniqueness and Additionality

Projects must also meet the criteria of authenticity, uniqueness, and additionality for eligibility to apply (under Article 10 of the Administrative Measures).

- Authenticity: This is the basic condition for applying for CCER. The Administrative Measures ensures that projects applying for CCER are authentic through a series of systems and measures:

- Project owners must publicise a series of supporting documents including project design documents before applying for project registration, in the validation and registration stage

- Third-party validation and verification body must validate and verify the authenticity of the project

- Preservation of original records of the data and information involved in the project design documents, as well as management ledgers, for at least 10 years

- MEE will organise inspections to verify the authenticity and compliance of registered projects and CCER, including the implementation, original data and relevant materials involved in the project design documents and accounting reports

- The project owner and the validation and verification body are potentially subject to legal liabilities if a registered CCER project engages in fraudulent practices, in addition to the possible revocation of the registered CCER project. This might include, but is not limited to, administrative liabilities such as fines, suspension of registration application, and revocation of qualifications for validation and verification. It could also extend to potential civil and criminal liabilities.

- Uniqueness: The project does not engage in other emission reduction mechanisms, preventing double registration of projects and double counting of emission reductions. In other words, the project is only evaluated once under one mechanism, to avoid violating principles of fairness and effectiveness. Project owners are responsible for ensuring projects have not applied to other emission reduction trading mechanisms, such as globally-recognised standards like the Verified Carbon Standard (VCS).

- Additionality: This is the crucial indicator of “emission reduction” for any carbon credit project evaluation. The project implementation must overcome financial, financing, key technology and other obstacles, and have an additional emission reduction effect compared with the baseline scenario determined by relevant methodologies. That is, the GHG emissions of the project are lower than the baseline emissions, or the GHG removals are higher than the baseline removals.

Any carbon credit needs to encourage and promote emission reduction projects that “have additional emission reduction effects” or “would not have been implemented” so as to achieve the goal of reducing global GHG emissions.

The assessment of “additionality” is a central issue in determining whether voluntary emission reduction projects can apply for carbon credits under relevant mechanisms. For a more detailed description and consideration of "additionality", see our insight Considering Carbon Credit Projects from the Perspective of “Additionality.”

Unified and centralised trading and related infrastructure

Under the renewed scheme…

- the National GHG Voluntary Emission Reduction Registration Authority (Registration Authority) is responsible for the operation and management of the National GHG Voluntary Emission Reduction Registration System (the Registration System).

- Akin to centralised registration in securities: the Registration Authority accepts applications for registration and deregistration of GHG voluntary emission reduction projects and CCER, records information, manages the registration, holds, changes and deregisters CCER, and issues relevant certificates upon application.

- Information recorded in the Registration System is the “ultimate grounds” for determining the attribution and status of the CCER. In other words, the finalisation of any trading from a legal perspective is based on the status change completed in the Registration System.

- the National GHG Voluntary Emission Reduction Trading Institution (Trading Institution – adopted by China Beijing Green Exchange) is responsible for the operation and management of the National GHG Voluntary Emission Reduction Trading System (Trading System).

- all CCER trading is conducted in the trading system, and all businesses and individuals interested in trading CCER are required to open an account in the trading institution. CCER’s OTC ceases to exist.

Validation and registration under ‘Approval System’

The renewed scheme includes…

- methodology development. This refers to the technical specifications used to determine the baseline, demonstrate additionality and calculate the emission reductions of GHG voluntary emission reduction projects in specific fields. Different voluntary emission reduction trading mechanisms may use different methodologies.

- Under the Administrative Measures, the MEE organises and formulates the CCER methodology with extensive public consultation. The MEE openly solicited methodological suggestions for GHG voluntary emission reduction projects in the form of "open-door decision-making”.

- The first project batch of methodologies has been released, in accordance with the principle of "release one when it is mature". Further progress regarding the assessment and selection process is also under way.

- third-party validation and verification bodies approved by SAMR and MEE.

- Only approved bodies (in accordance with the Certification and Accreditation Regulations) can engage in the validation and verification of CCER.

- The Administrative Measures clarify the code of conduct for validation and verification bodies, the regular work report system, the prohibition of staff members of validation and verification bodies from participating in CCER trading and other activities that may affect impartiality.

- The Validation and Verification Technical Committee will coordinate and resolve technical issues related to validation and verification, and to enhance the consistency, scientificity and rationality of validation and verification activities. The fairness of the validation and verification process is enhanced through prior admittance and a series of monitoring measures during and after the process.

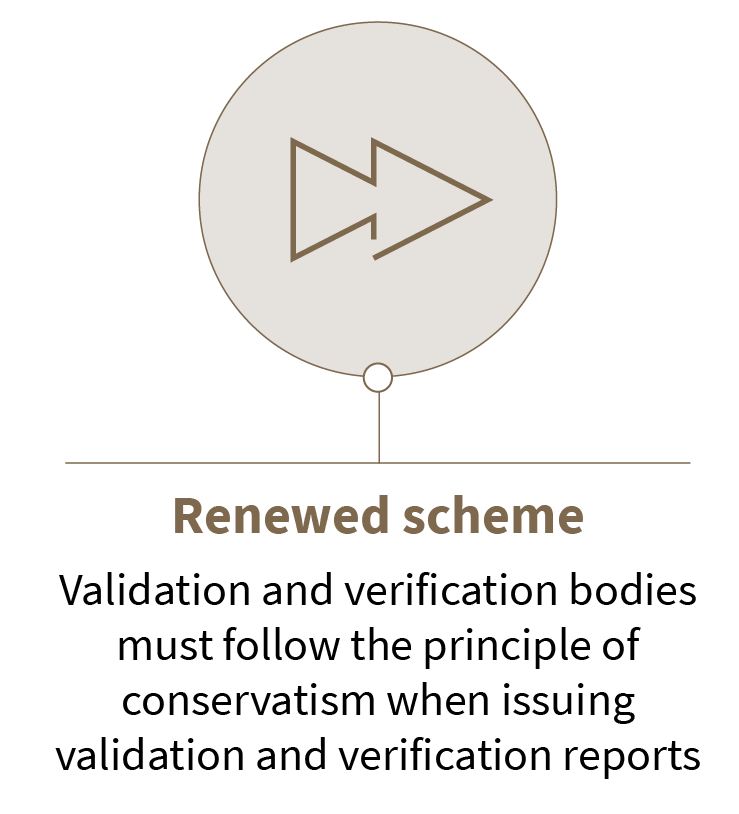

The Principle of Conservatism

The ‘principle of conservatism’ refers to taking a conservative approach in estimation, valuation and other measures, to ensure the project’s emission reduction is not over-calculated. In other words, in the face of technological uncertainty, the validation and verification bodies should adopt a cautious and conservative attitude.

- This is to account for any uncertainties or lack of effective technical measurements, which can make it difficult to accurately judge relevant parameters and technological paths.

- This requirement is also intended to maintain the fairness of the CCER issuance process and to avoid damage to the market credibility of CCER due to excessive or improper issuances of CCER.

Outlook – more trading, innovation and potential cross-border participation to come

We are confident the CCER scheme will successfully restart. We expect it will make significant progress once officially relaunched, including:

- Significant increase in transaction volume under centralised trading

One of the key changes from the restarted CCER scheme is the consolidation of scattered pilot trading exchanges across the country and over-the-counter transactions into a single unified market. As the launch of the renewed CCER scheme, we expect the transaction volume and frequency of CCER to increase significantly compared with the CCER trading market before 2017.

Having a sustained and stable trading volume and forming a representative settlement price will encourage the CCER market to develop:

- participants can accurately predict the cost of CCER purchase like other mature trading products

- having representative prices is conducive to innovation, including the development of CCER-based financing and risk management derivatives in the future.

- Potential cross-border trading(watch this space)

- International investors are curious to understand whether carbon products in China's carbon market can be traded across borders. The Administrative Measures stipulates that “the specific provisions for cross-border trading and usage of CCER will be separately formulated by the MEE in conjunction with relevant departments.” In other words, the cross-border trading of CCER needs further clarification by legislation. Innovation of trading methods, introduction of financing and derivative products to enhance market vitality

The Administrative Measures enables spot trading methods such as listing agreement, bulk agreement and one-way bidding. We look forward to more efficient and flexible CCER trading methods in the future.

In addition, with the maturity of spot transactions, the demand for CCER-based financing and derivatives will gradually emerge. Market participants are increasingly in need of financing tools to revitalise their carbon assets, and of derivatives to complete necessary risk management and hedging.

We expect the restarted CCER market to become a more mature and dynamic trading market, fully unleashing the core value as a carbon pricing policy tool and helping China to steadily achieve its ‘30.60’ target.

Visit the original Chinese version of this update here.